YC's got a space strategy

And they're not a bunch of space cadets!

YC, or Y Combinator, is probably the world’s best known startup accelerator program.

If it isn’t, it certainly deserves to be, because it has a well-deserved reputation as the best startup accelerator program in the world. Based on the historical plot below, it’s not a particularly close call.

They’re better at identifying unicorns at this super-early stage than anybody else in the business.

Lars Osborne, the Chief Engineer at Agile Space, specifically asked about YC’s performance in the space sector on X last week — and it piqued my interest.

When I pressed him for whether he thought technical or financial performance was more critical in the assessment, he had an incredible response:

Both.

Gains without a good technical foundation are just a bubble. Technical merit that doesn't produce value is typically an execution problem.

What space startups has YC backed?

To kick things off, here’s a list of the startups YC has backed that I see as operating (or planning to operate) in space, and what they’re working on:

W15 Bagaveev Corporation - small satellite launcher1

W16 Astranis - next-gen internet satellites in geostationary orbit

W16 Relativity Space - 3D printed, methalox-propelled heavy-lift launch vehicle

S16 Prime Lightworks - electric propulsion for satellites

S17 Tesseract - chemical thrusters for satellites

S18 Momentus - last mile transportation for small satellites2

W19 SpaceRyde - on-demand delivery in space3

S19 Epic Aerospace - last mile delivery for satellites

W21 Alba Orbital - commercializing the pocketqube satellite form factor

W21 Albedo - satellites in very low earth orbit capture optical and thermal images

W21 Care Weather - high accuracy global weather data from cheap spacecraft

W21 Stoke Space - 100% reusable super-heavy lift launch vehicles

S21 HEO Robotics - taking pictures of spacecraft

S21 Inversion Aerospace - space-to-ground cargo vehicles

S21 TransAstra Corporation - asteroid mining

S21 Turion Space - moving things around in space, taking pictures of spacecraft

W22 AstroForge - asteroid mining

W22 Hubble Network - space-to-device Bluetooth connections

W22 KorrAI - tracking ground movements from space

W22 Wyvern - high-resolution hyperspectral imaging

S22 Array Labs - satellite-driven real-time 3D map of the world

S22 Quindar - monitor and automate satellite ops (SaaS)

S22 Velontra - hypersonic space plane

S23 Orbio Earth - tracking oil and gas industry methane emissions from space

W24 Basalt Tech - automate satellite operations (SaaS)

W24 Elodin - future of aerospace software (SaaS)

W24 Navier - machine learning for computational fluid dynamics (SaaS)

S24 Lumen Orbit - building space-based data centers

S24 Spaceium - fully automated space stations to refuel/repair spacecraft

For an accelerator that’s not a sector specialist, my initial impression is that this is a remarkably long list!

Of particular note, I’m not going to consider startups with the following types of products in the following analysis:

Software startups5

Ground segment hardware startups

Startups that produce aerospace systems that only operate in the atmosphere

Financial Performance

Financial performance in a firm that’s still operating as a startup is often difficult to assess from the outside because unlike public companies, they don’t have to share what they’re worth, or who owns them. For these plots, I collected data from PitchBook; inaccuracies in that data will be represented here as well.

Let’s start with some easy numbers:

24 YC-backed space hardware startups are part of this data set (though not all will be present throughout due to unavailability of certain data).

1 YC-backed space hardware company has gone public so far; it used a SPAC.

2 YC-backed space hardware companies have gone out of business so far.

One thing is quickly clear from this: based on past performance, if a founder gets into YC as a founder in the space sector, their odds of raising a seed round go, well, to the moon. This isn’t unique to the space sector; that’s part of YC’s value proposition.

The only space hardware companies who haven’t done that yet either went through YC during COVID-19, or are still going through YC. I’ve heard that YC-backed companies are having a more difficult time raising institutional seed rounds, but I don’t think this will affect space startups as severely because the minimum capital requirements are so much larger.

The other thing that I find interesting about this is that most companies are following, +/- 1 year, the conventional “raise a round every 2 years” approach to fundraising. Most of the companies within 2 years of their batch have raised a seed round, most within 4 years have raised at least a Series A. The pattern gets a bit spottier as one looks farther back, but pre-pandemic the data gets a lot more sparse.

While YC makes it easier to raise a seed round, and might lead to a higher cap or valuation for early-stage investments, it does not seem to significantly affect the pace of future fundraises. This surprised me, as I thought hardware startups might raise on a different schedule due to different capital requirements from SaaS.

What does this second plot show?6

First, YC found unicorns in Astranis, Relativity, and Momentus — all 3 had at one point unicorn valuations, and all 3 were early investments in the sector.

Second, a number of these companies that have done well haven’t exited at or held their peak valuations. That should be a caution flag to investors in the sector not so much about YC, but about the ability of space companies to keep their valuations sky-high as their technology matures and they become companies that have to sell a real service or product. I think the startups, founders, and investors most at risk here are the ones engaging with round sizes that are significantly higher than market terms. This isn’t so likely to be an issue for YC itself since they have a standard deal, but could be problematic for a lot of investors who come in after YC.

Technical Performance

Alex Iskold, GP at 2048 Ventures, posted recently on X about YC:

YC thinks that what matters is smarts and drive and FMF is secondary.

It worked for them quite well because of stage and cost per point.

Mostly everyone else invests in FMF.

I think all three qualities are necessary, but not sufficient, for early-stage space hardware startups to succeed. What I think they’ve historically needed the most at the earliest stages is the synthesis of a vision for the future with great engineering. That’s what enables the ones that make it to build awesome new technologies that customers need.

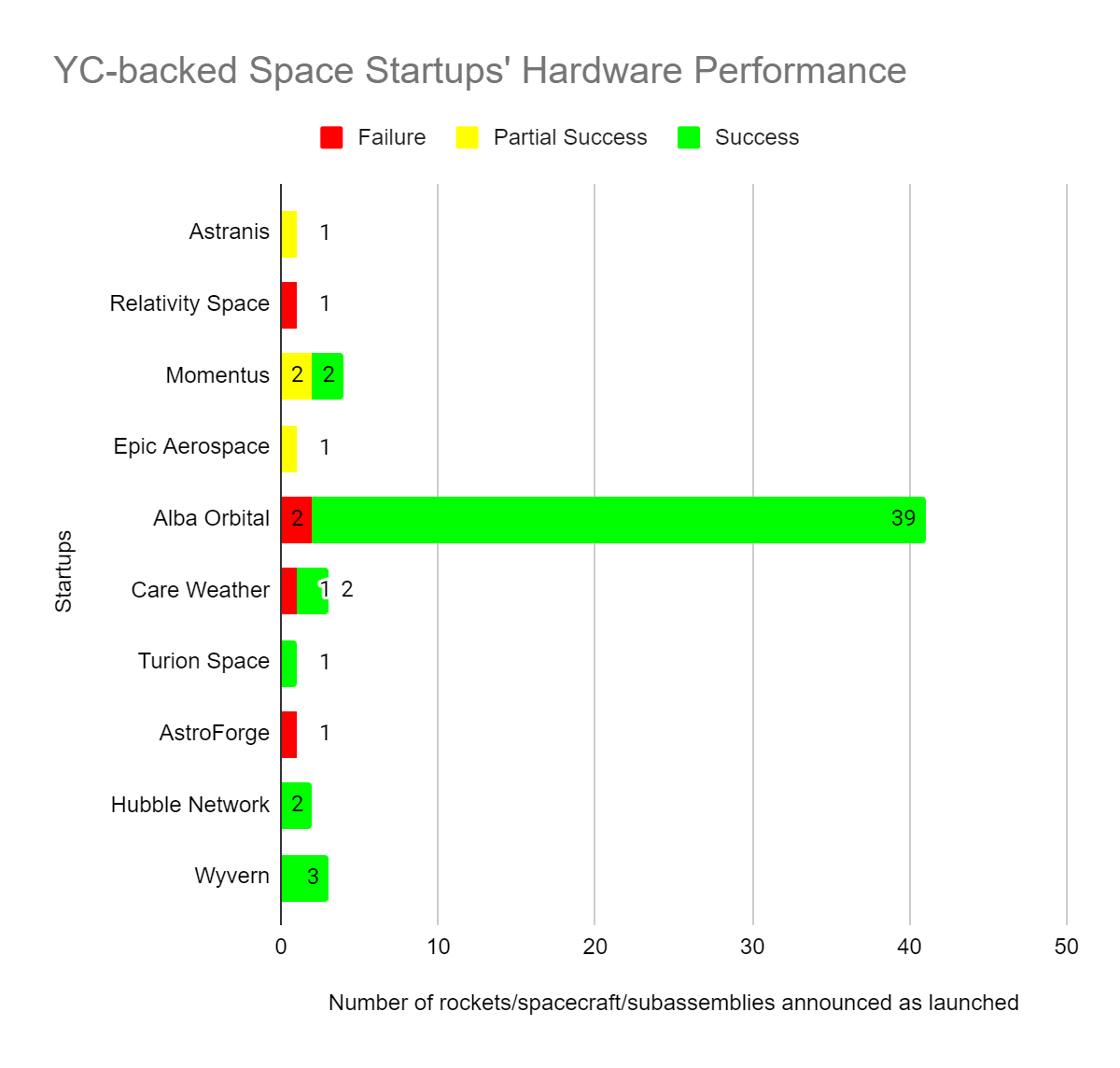

Technical performance here seems fairly easy to check. YC’s messaging to current and future founders is to make “something people want”. So my initial heuristic for this among the hardware companies was as follows:

How many complete systems have they launched?

How many complete systems have they launched that customers have used?

How many complete systems have they launched that met their mission objectives?

I put together a chart based on what I found from Wikipedia and company websites. All startups not on this chart, as far as I can tell, haven’t flown hardware yet.

In the process of constructing the chart, it became clear that my initial approach…didn’t work. Here’s why:

When counting launches, the question of “what counts as space?” is a contentious issue that’s potentially worth its own post and I don’t want to dive into. It also doesn’t differentiate between the costs of hardware — a pocketqube startup is going to have far more shots on goal than a heavy-lift launch vehicle startup, because the cost of building hardware to try again is different by multiple orders of magnitude.

Focusing on customers when evaluating early-stage startups that need to prove out new hardware ignores that customers often have requirements for flight qualified systems; a launch without customer payloads could actually move an early-stage startup as far along in terms of demonstrating readiness and justifying a new valuation as flying a customer payload.

Using mission objectives started to feel like bad analytics, because missions and their outcomes are self-reported.

What can I say about technical performance?

I might have thought that, as a group, older startups would be more likely to have more launches under their belt. Due to the varying types of hardware pursued by YC-backed space startups, this is not the case.

The plot does show that older startups are more likely to have launched hardware, but that’s fairly intuitive — even today it takes some amount of concentrated technical effort to build spaceflight-worthy hardware, and if a startup is doing something that’s VC-backable, that R&D effort will likely take some time.

Going back to look at the prior chart as well, launching hardware into space tends to drive up the value of a startup if its low, but could actually hurt it in two cases. If the hardware doesn’t work, that’s typically a problem. Most space startups don’t have the money for all that many launch attempts, so a failure, even a partial failure, for really any reason on an early flight can cause issues for a company at any stage. The second is if the startup already has a sky-high valuation. In this case, following financing rounds seem to become less about the startup’s potential, and more about its monetization opportunities.

Perhaps least intuitively, flight failures are not, as of now, associated at all with startup failures among YC alumni. All YC-backed space hardware startups that have failed so far have failed before flying anything. By the time a space startup launches hardware, regardless of whether it’s YC-backed or not, it’s operating under the impression that it has reduced the technical risk to acceptable levels. So even if the hardware doesn’t work exactly as designed, if it’s clear where and why the failure occurred, the technology risk is still in a great spot compared to where the startup was when YC invested.

Based on the chart, the startups I’m most intrigued by are Hubble Network and Wyvern. They’ve had early operational successes, and have interesting technical stacks with a clear path to providing value to users on earth from space.

Why YC’s approach is smart

YC announced yesterday that they’re changing their strategy; instead of two large cohorts per year, they’re going to run four smaller batches each year going forward.

YC batches have grown radically in size since the program started. Jared Heyman wrote a great post on this trend from 2005-2022. YC’s W24 batch had 260 startups, and it looks like their S24 batch has 256 as of today. This is lower than the historical peak, and higher than most ZIRP-era batches.

From YC’s 2015-2020 batches, they found 3 space startups that were at one point unicorns. Going 3 for 7 on space hardware investments in that 5-year period is significantly higher than their general unicorn hit rate from that era of around 4%. So planning to include some small number of space startups in many batches going forward is a particularly smart move on their part.

As the space industry matures, I’m very curious to see where YC thinks the next innovations in the field are going to be!

Out of business.

Out of business.

My friend Ian wrote a Substack post about the space startups of the S21 batch that I highly recommend.

SaaS startup progress is measured so differently from hardware startup progress that I don’t think comparisons between them as-is are particularly meaningful, and I can’t come up with a general approach to converting between them whose accuracy I’m satisfied with in a week.

The basis for this plot is the last raise in a year on PitchBook that closed and had a post-money cap or valuation.

love this aaron !!