Where do great defense startups go?

The NatSec100 2026 Edition

The Silicon Valley Defense Group (SVDG) published its 2026 NatSec100 list last week. It tracks “the top 100 venture/PE-backed American defense companies that are innovating, building, and delivering warfighting capabilities”.

Similar lists were published in 2025, 2024, and 2023, which makes comparative cohort analysis meaningful. Since 2023, there’s been many opportunities for new companies to win contracts, even over multi-year procurement cycles. Furthermore, the technology that’s in vogue with private markets investors has changed significantly. The defense industry has gained a lot of momentum with investors since the first list. The relative importance of technical fields within the defense industry has also been dynamic over this time period.

This week I’m exploring changes in the NatSec100, and what’s happened to the 216 firms which have been named to it since it was created.

What does the list mean?

The list is developed using a proprietary quantitative method. While we don’t know the weights, key factors include indirect indicators of operational traction, capital formation, and growth. These startups are outperforming in terms of operations, raising funds on the private markets, and in getting big. Specific indicators include:

US government contracts

Recent capital raised

Total capital raised

Recent headcount growth

The idea at the root of this is that all great growth-stage startups selling to governments have some sort of publicly available information about all of these things. That makes it possible to draw comparisons across stage, specific business model, and sector within the national security—from quantum technologies to AI tools to high-speed drones.

Through this list, SVDG is tracking momentum among successful startups, more than absolute outcomes. Because substantial momentum as a late stage startup is rare, inclusion on this list for multiple years is evidence that a still-private startup is doing great. Momentum is also a KPI for the largest customer in the industry.

The inclusion criteria for the NatSec100 represent a dynamic and relatively broad definition of defense tech success stories. They are also continuously refined; a spot on the 2023 list and a spot on the 2026 list don’t mean exactly the same thing. The most significant change in 2026 is a new partnership with Pryzm, which unlocked government government contracting data as a direct input to the rankings for the first time.1

Startup Origin Stories

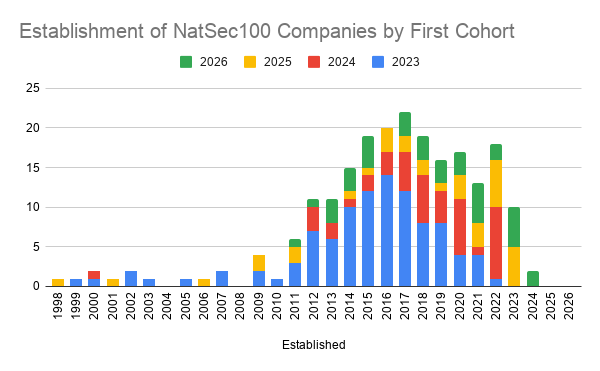

SVDG seems to care a good deal about where in the country the startups in their list come from, and they track this in each report both through the table and an infographic.

SVDG also tracks when each startup is founded in the reports’ company tables, but they don’t make the data easier to analyze with a nice picture. So I made one.

The plot above shows when companies listed in the NatSec100 were established, colored by their first cohort, when they were first added to the list (so a company present in 2024 and 2025 is counted in only the 2024 list).

The mid-2010s were a great period to start a defense company; the top four years by number of companies are 2015-2018. That’s about when the commercial space sector took off, machine learning and natural language processing became big, and R&D resources became available for quantum technologies.

2022 was also a really great year to start a defense company, probably because of the generative artificial intelligence developments around that time.

I can understand why this isn’t something the report dwells on, despite the significant impact it has on startup (and VC fund) outcomes. Vintage year simply isn’t something that founders or their direct investors have meaningful control over. Furthermore, the report is less focused on early-stage companies than on the succeeding startups that stand to move the needle with their national security government contracts.

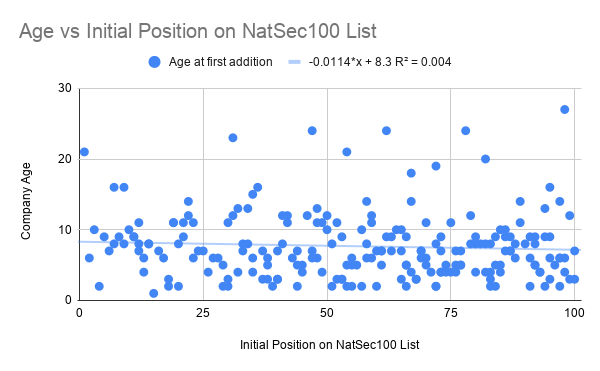

The other question I had about this was whether there’s a relationship between startup age and initial position in the rankings when a startup joins the NatSec100?

Looking across all cohorts in the chart above, older startups do not join closer to the top of the list. An R2 of 0.004 is negligible.

I write Molding Moonshots in a personal capacity.

If you are building in deep tech and thinking about raising Pre-seed, Seed, or Series A funding, I’d be more than happy to have a chat on professional terms, as an investor at MFV Partners!

Send me an email and we’ll find a time.

Where do these startups go?

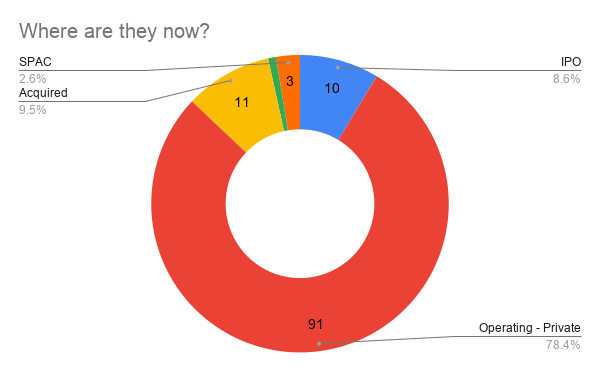

Each year, there is significant turnover in the NatSec100. Of the 216 startups who have been on the list at some point, 100 are still on the list—either for the first time, because they’ve stayed on, or because they were added back after departing.

The chart above tracks the current state of the startups which appeared on past versions of the list, but were not included in the 2026 NatSec100.

The overwhelming majority of firms that dropped off the list are still operating as private companies. Once a firm gets big enough to join this list, it’s not going to mark to $0. It might not return the fund, or even all the capital it’s raised, on the timeline a VC would like—but it’s likely got a right to continue existing under some ownership structure. It’s hopefully got a path to profitability.

It’s certainly big and valuable enough that somebody will pay something to acquire it. And that’s exactly what happened at 11 of these companies, representing just under 10% of the sample.

About 11% of the firms mentioned on the list have dropped off for the best reason possible; they have gone public. This is clear evidence value creation for their investors, and more importantly for their employees.

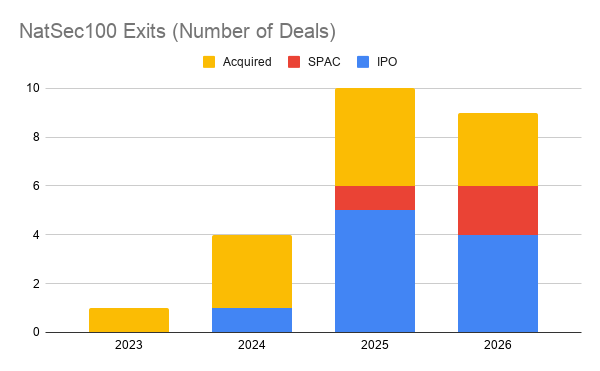

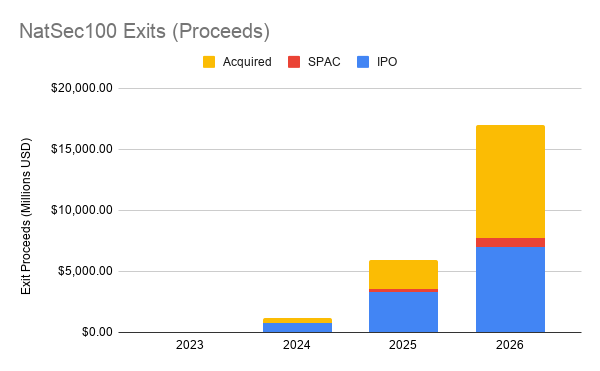

The next important question is when these exits occurred? This is probably a meaningful fraction of the VC-backed defense sector’s late-stage M&A over the past few years, so understanding the dispersion of these 24 transactions might provide some insight into the health of the field.

The chart above shows when startups which used to be in the NatSec100 exited, either through acquisition or by going public.2 It’s essential to note that not all of these are VC exits. Some of these are exits from buyouts of one kind or another.

The number of late-stage deals is clearly up, which is good for the health of the ecosystem. It shows an IPO window of sorts is very much open, and that successful startups with national security customers can certainly get big enough to IPO. SPACs are also making a come-back.

The chart shows aggregate exit proceeds are taking off, well, like a rocket.3 Exit proceeds this year have blown past 2025, even though fewer deals have been done so far (and as SpaceX’s IPO hasn’t generated proceeds yet, it is not included).

The IPO window looks wide open to me.

The IPO that generated the most proceeds was BETA Technologies in 2025, which brought in $1.01B, but the most expensive exit to date has been Armis, which ServiceNow acquired for $7.75B earlier this year. IPOs and acquisitions generated extreme variation in proceeds. The average IPO brought in $683M, about $130M less than the median IPO. The average acquisition brought in about $1.2B, more than 3x the median acquisition. Some acquirers are clearly happy to pay a premium.

SPACs are coming back, but are both less popular and experience less extreme variation in the proceeds, generating $200-550M including the PIPE.

Who has staying power?

Startups on the list in 4 years, every year so far, include Anduril, Databricks, Sierra Space, Chainalysis, Axiom Space, Grafana Labs, Shield AI, Skydio, Scale AI, Lyten, DataRobot, PsiQuantum, Stoke Space, Applied Intuition, Epirus, Impulse Space, Astranis, Whoop, Lambda, Vannevar Labs, Hermeus, X-Bow, CesiumAstro, and Varda Space.

Startups on the list in 3 years include SpaceX, Relativity Space, Dataiku, SandboxAQ, Dragos, Ursa Major Technologies, ThoughtSpot, SambaNova Systems, Blue Origin, Cerebras Systems, VAST Data, Loft Orbital, SiMa.ai, BigID, Firefly Aerospace, Nozomi Networks, Gecko Robotics, Automation Anywhere, Second Front Systems, LeoLabs, Snorkel, Regent, Apex Space, K2 Space, Hadrian, Horizon3.ai, Nominal, Onebrief, Saronic, Tomorrow.io, Radiant Nuclear, Umbra Space, True Anomaly, and TRM Labs.

Startups on the list in 2 years, at least one of which was this year, include Slingshot Aerospace, Saildrone, RED 6, Ayar Labs, Forterra (formerly RRAI), Boom Supersonic, Shift5, Re:Build Manufacturing, Firestorm, Dataminr, Castelion, Chaos, Strider, Cape, Ditto, Overland AI, Turion Space, Virtualitics, and Govini.

This kept OpenAI and Anthropic off the list in 2025, and Anthropic off the list in 2026.

This chart considers SpaceX as IPOing in 2026.

Where transaction terms are not disclosed, the proceeds recorded are $0. Not all proceeds in this chart are actually equal—for example, it treats USD across years, foreign currencies converted to USD, and stock as equivalent when these things aren’t.