Is Biotech Deep Tech?

Do drug discovery startups belong in deep tech portfolios?

Last week I went to Ann Arbor, MI, where I watched one of my brothers defend his PhD dissertation. It was an absolutely inspiring experience.

Congratulations on passing your defense, Dr. Pickard!

This Dr. Pickard studied computational biology, or bioinformatics, so I’ve been thinking about the biotech industry recently.

As Wikipedia defines it, “Biotechnology is a multidisciplinary field that involves the integration of natural sciences and engineering sciences in order to achieve the application of organisms and parts thereof for products and services.[1] Specialists in the field are known as biotechnologists.”

Gus Domel at Boost VC posted on LinkedIn about a month ago asking why deep tech investors seem to shy away from investment candidates in biotechnology. He challenged readers:

Why don't a lot of deep tech investors include Bio as deep tech? Investors tend to define deep tech as a company that takes technical risk, rather than market risk. Is this not exactly what Bio is? If you cure an important disease or create a great tool that aids in that, there is a market waiting on the other side of that without question.

This framing, as well as Wikipedia’s definition, bring drug discovery to the top of my mind; this post will consider that as generally representative of biotech.

{kind=link}

Around the time Gus posted on LinkedIn, Daniel Yang at Lux Capital made an interesting point about the biotech industry on X. It doesn’t seem to have been posted in a direct response to Gus, or even in the same immediate context, but it speaks to his question:

Biotech is an industry of permissions. Permission from investors to do R&D for your idea, permission from FDA to run your trial & market the drug.

This is a major frustration to newcomers, especially those from tech where agency & sheer will can bend the rules and be rewarded

What Daniel’s getting at here is that technical progress in biotech does not necessarily unlock market access. It is quite possible to make massive and fast progress in the technology, and have to wait for permission to enter the market.

In most other deep tech sectors, there’s this belief that if you build it, customers will come. That does apply to biotech, but only after the founders receive regulatory approval.

On the other hand, if regulatory approval is received, then a biotech startup is nearly assured of a successful exit. Deep tech doesn’t have that sort of pattern.

If you invest in startups, like my writing, and want to chat about possible career opportunities, don’t hesitate to be in touch. The best way to get ahold of me is via email:

Differences

The regulatory processes Daniel mentioned, and that reduce biotech market risk, come across as idiosyncratic to investors who have a deep tech background but aren’t specialists in biotech. There’s not really anything else like them in the US where the scientific risk must be mitigated through non-recurring engineering, and only afterwards does the government tell you whether or not you’re allowed to sell the product.

Furthermore, these regulatory approval processes are pretty close to all-or-nothing. It’s possible to remove almost all of the technical risk and still get blocked by regulatory authorities. Of the cases where I’ve heard of that happening, they didn’t redo the trial that didn’t get approval — they switched drug candidates and started over at the beginning of what the FDA calls clinical research (or even pre-clinical research) — or they went out of business.

To be clear, this isn’t a bad thing. I’m also not saying the government should do it differently — human lives and trust in the medical system are at risk if the FDA gets this wrong. It is just very different from the regulatory processes I’m familiar with. If the FAA or FCC didn’t like a spacecraft communications plan, my colleagues typically didn’t have to do a clean sheet redesign of the whole satellite.

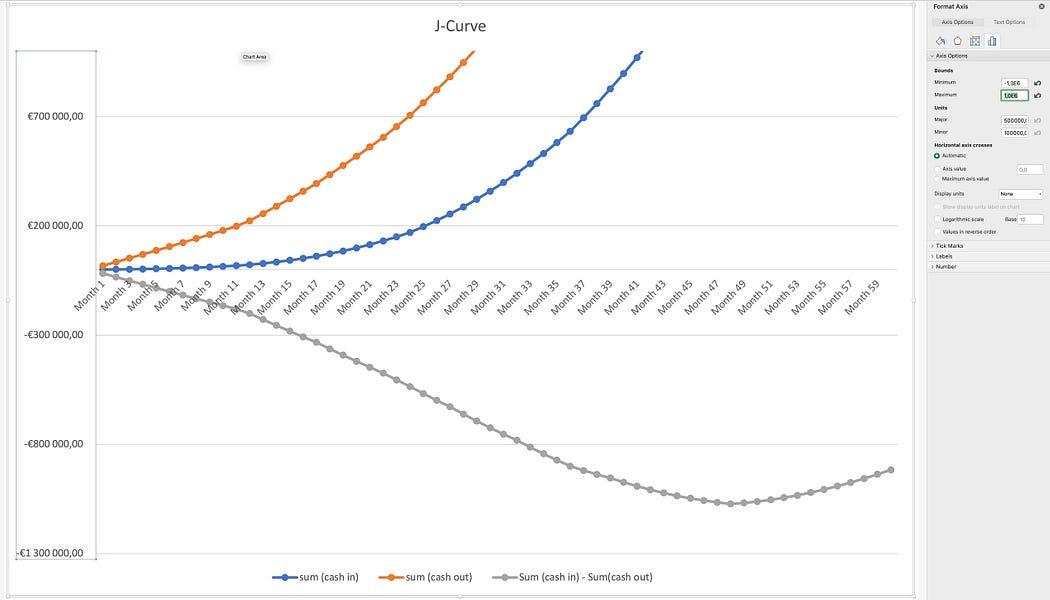

The other key difference is about cash flow timing. In a Medium post, Rodrigo Sepulveda Schulz talks about the concept of the J-curve. While the piece is written for a European audience in the sense that it’s Euro-denominated, he does an excellent job walking readers through cash consumption of a startup, which is what the J-curve represents.

Earlier today, Aaron Zucker at Sapir Venture Partners published a Medium post arguing that the J-curve in deep tech investments will likely look different from other VC strategies.

I’m not certain I agree with all of Zucker’s points, but I find his idea that the deep tech curve will look different, and how it will look different, compelling.

I think that the minimum value on the J-curve will be even more extreme in biotech than it will in generalist deep tech, for two reasons:

due to the expense of pre-clinical and clinical trials, the total cash needs in biotech may be more than in other areas of deep tech, so the trough of the curve will be farther from $0

due to the time required to conduct these trials, the startup will not start to generate cash until far later than the plot shows for standard startups, or even deep tech startups

This isn’t saying I think the outcomes will necessarily be better when the value becomes positive — only that I think the average biotech startup will require more capital before it starts generating cash than the average deep tech startup.

This isn’t a problem unless the capital markets say so, and private markets seem to accept this state of affairs quite happily. It’s very possible for a drug discovery startup to get acquired pre-revenue.

Similarities

It’s also important to note that biotech is similar to deep tech in some key ways.

Unlike, say, Enterprise SaaS, purchasing processes in deep tech and biotech tend to be complex. The user is often not the same individual as the buyer, and may not even be in the same organization. This creates lengthened acquisition processes with multiple levels of approval. In turn, this creates space for rent-seeking agents to be involved in the sale and use processes.

Biotech and deep tech also share a need to engage seriously with ethics. In deep tech, this is perhaps manifesting most seriously in conversations about the potential of AI and the responsibilities of AI developers. In biotech, the ethical questions seem to be somewhat more developed, because they’re tied to longstanding conversations around medical ethics. A particularly salient series of issues for founders and investors relates to drug costs. I believe quite strongly in the potential of both sectors to produce ethical outcomes, but investors and founders across both fields need to think seriously about the implications of their work.

Both sectors also share long R&D cycles. Ali Alam, out of Blackstone, said on Medium that deep tech startups often take 5-10+ years to bring a product to market. Bessemer Venture Partners’s XB100 list has an average age of 9.2 years old, $801 million in capital raised on average, and an average valuation of $4.4 billion. N-Side says that during the 2010s, it took on average 10.5 years for a medicine to go from discovery through regulatory approval (averages for specific fields of medicine ranged from 9.2 to 12.2 years), but that’s on the low end of some other estimates. V-Bio Ventures, a European fund, corroborates this and says that the time to develop a new drug is still increasing. The fund identifies some key reasons as:

increasing regulatory complexity

rising capital requirements

While both biotech and deep tech have long R&D cycles, biotech startups can take a particularly long time to launch their product and start generating revenue.

Macro Views

V-Bio Ventures also indicated that macroeconomic uncertainty and exit challenges (the IPO window has been closed for much of the past decade) contribute to longer biotech startup R&D cycles.

David Li, a cofounder of Meliora Therapeutics, made a very important point about the macroeconomic environment on X last month:

another case in pt how this downturn in biotech is different >>

biotech as an industry has pretty much only existed in a falling rates regime

we're finding out how venture math for long-dated biotech cash flows works if cost of capital is increasing rather than decreasing over time

I’m certainly not in a better position than he is to predict where things go from here, but we do seem to be in uncharted territory.

This seems particularly important in the context of the J-curve, and the specific financial products (in terms of fund lifetime, among other things) that VC General Partners are selling to their investors.

Final Thoughts

I can’t get away from the timing of cash flows in biotech vs deep tech. Most other deep tech startups will be able to sell something — a prototype, a component, a scaled-down version, even consulting services if they have to — within 10 years. Biotech startups often can’t. Biotech investors and founders have got to be in it for the long haul.

So I think that where Gus invests (in pre-seed rounds, at a target rate of one investment/week), biotech is absolutely deep tech. Biotech could certainly belong in an early-stage deep tech portfolio, when nobody in deep tech insists on seeing any sort of revenue to consider a company investable.

But after the stage where a deep tech investor outside of biotech might want to see revenue, biotech seems like a totally different game.

Consequently, the mid-stage and late-stage network an awesome early-stage investor should have probably do not look very similar across the two fields. As a result, I think it’d be very difficult for an individual to be both a world-class biotech investor and a world-class deep tech investor.

To answer Gus’s question directly, I think it’s so hard for one person to be very well networked and knowledgeable enough about both deep tech and biotech that most investors don’t want to try to be world-class in both, and prefer to focus on one or the other.

While I think it’s highly unlikely that one person will be world-class at both, that does not seem like such a big issue at the fund level.